World

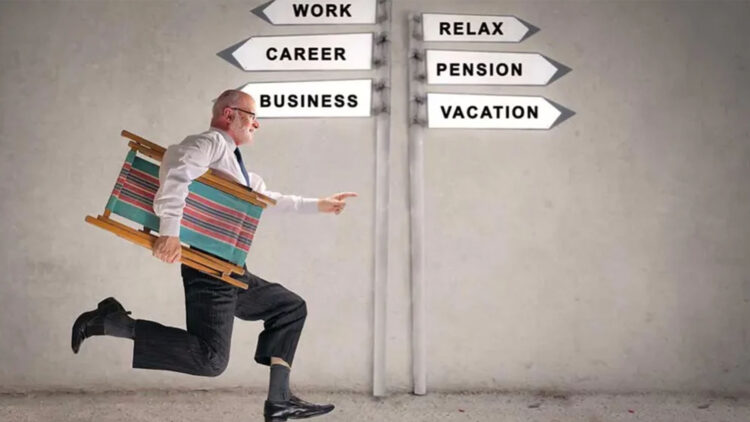

Retiring Early? It Could Slash Your Social Security by 30%

Many individuals considering retirement at ages 62 or 63 may face significant financial repercussions. Recent analyses reveal that choosing to retire at these ages could reduce Social Security payments by up to 30%, impacting long-term financial stability for millions in the United States. This shift in understanding is critical as it challenges the traditional perception of the “ideal” retirement age.

Research indicates that the average retirement age for Americans is currently around 62. This is also the earliest age at which Social Security benefits can be claimed. Despite this, surveys, such as the one conducted by MassMutual, suggest that many people still view age 63 as the optimal target for retirement. However, this perspective may need reevaluation given the evolving landscape of Social Security, health care costs, and life expectancy.

Understanding the Risks of Early Retirement

The full retirement age (FRA) for individuals born after 1960 is 67 years old. Only at this age can retirees access their full benefits. According to the Social Security Administration (SSA), claiming benefits at 62 results in monthly payments that are approximately 30% lower than what would be received at full retirement age. This reduction remains in effect for the remainder of the retiree’s life.

In addition to financial implications, early retirees may face heightened health care expenses. Medicare eligibility begins at age 65. Therefore, those retiring at 62 or 63 may need to purchase private health insurance, leading to further financial strain during the initial years of retirement.

The average life expectancy in the United States is now approximately 78.4 years, with many individuals living into their 80s or 90s. This reality necessitates careful financial planning, as retirees need their savings to last potentially 20 to 30 years. Research shows that about 35% of those nearing retirement feel they do not have sufficient savings to retire at their preferred age, raising concerns about running out of money.

Strategies for Financial Security in Retirement

Given the uncertainties surrounding Social Security and personal savings, experts recommend supplementing retirement income beyond Social Security benefits. This can involve starting investments and saving as early as possible. Common retirement savings tools include:

– **401(k)**: Offered by many employers, these plans allow for pre-tax contributions, often with employer matching.

– **Traditional IRA**: A personal retirement account where funds grow tax-deferred until withdrawal, at which point they are taxed as income; contributions may be tax-deductible.

– **Roth IRA**: Similar to a Traditional IRA but funded with after-tax dollars, allowing for tax-free withdrawals in retirement.

– **TSP (Thrift Savings Plan)**: A retirement savings plan for federal employees and uniformed service members, similar to a 401(k).

– **Pension**: Though less common today, some employers still provide guaranteed monthly payments upon retirement.

Delaying retirement can provide additional years for saving and investing, enhancing financial security. Nevertheless, not everyone has the luxury of choice. Health issues or job loss may necessitate early retirement for some workers.

The notion that 63 is the ideal retirement age may be outdated, especially as individuals live longer and work healthier. For those who remain capable and willing to continue working, postponing retirement could lead to greater financial freedom in the long run.

For younger generations, early financial planning is essential. The sooner one starts budgeting and saving, the greater the options available in the future.

Shark Teeth Research Reveals Urgent Need to Protect Species

Church Members Unite in Resilience After Thanksgiving Fire

Community Unites to Attempt World Record for Largest Cookie Exchange

Mayor Lurie Appoints Alan Wong to District 4 Seat Amid Controversy

Mayor Appoints Alan Wong as New Supervisor for District 4

UK Report Reveals AI’s Role in Evaluating University Research Quality

Gabriela Jaquez Shines as No. 3 UCLA Dominates No. 14 Tennessee

Trump Promises to Release MRI Results Despite Uncertainty on Scan

Japan’s Q3 Capital Expenditure Slows Despite Surge in Profits

University of Hawaiʻi Joins $25.6M AI Initiative to Monitor Disasters

Toledo City League Announces Hall of Fame Inductees for 2024

DOJ Seizes $15 Billion in Bitcoin from Major Crypto Fraud Network

Sharp Launches Five New Aquos QLED 4K Ultra HD Smart TVs

Celtics Coach Joe Mazzulla Dominates Local Media in Scrimmage

Mutual Advisors LLC Increases Stake in SPDR Portfolio ETF

Community Unites for 7th Annual Walk to Raise Mental Health Awareness

Western Executives Confront Harsh Realities of China’s Manufacturing Edge

Major Networks Reject Pentagon’s New Reporting Guidelines

-

Science4 weeks ago

University of Hawaiʻi Joins $25.6M AI Initiative to Monitor Disasters

-

Lifestyle2 months ago

Lifestyle2 months agoToledo City League Announces Hall of Fame Inductees for 2024

-

Business2 months ago

Business2 months agoDOJ Seizes $15 Billion in Bitcoin from Major Crypto Fraud Network

-

Top Stories2 months ago

Top Stories2 months agoSharp Launches Five New Aquos QLED 4K Ultra HD Smart TVs

-

Sports2 months ago

Sports2 months agoCeltics Coach Joe Mazzulla Dominates Local Media in Scrimmage

-

Politics2 months ago

Politics2 months agoMutual Advisors LLC Increases Stake in SPDR Portfolio ETF

-

Health2 months ago

Health2 months agoCommunity Unites for 7th Annual Walk to Raise Mental Health Awareness

-

Science2 months ago

Science2 months agoWestern Executives Confront Harsh Realities of China’s Manufacturing Edge

-

Politics2 months ago

Politics2 months agoMajor Networks Reject Pentagon’s New Reporting Guidelines

-

World2 months ago

World2 months agoINK Entertainment Launches Exclusive Sofia Pop-Up at Virgin Hotels

-

Science1 month ago

Science1 month agoAstronomers Discover Twin Cosmic Rings Dwarfing Galaxies

-

Top Stories1 month ago

Top Stories1 month agoRandi Mahomes Launches Game Day Clothing Line with Chiefs